European Central Bank officials will debate a quarter-point interest-rate increase on Thursday, and the decision could go either way.

It’s looking likely that the dynamics of the meeting in Frankfurt will determine whether policymakers opt for a 10th consecutive hike in borrowing costs or choose to pause, along with delivering a probable message of hawkishness.

While the decision is the most suspenseful since the ECB began its tightening campaign more than a year ago, investors have proven hard to persuade that another move is imminent. Dutch official Klaas Knot, in an interview on Wednesday, suggested that markets were “maybe” underestimating the prospect of a hike.

The quandary he and his colleagues face is whether inflation — still stuck above 5% — can definitively slow without more tightening, given increasing evidence of the eurozone economy’s weakness and the lag with which policy moves have an impact.

What Bloomberg Economics Says:

“We forecast the Governing Council will push through a 25-basis-point increase for a final time in this cycle, bringing the deposit rate to 4.0%.”

—David Powell and Maeva Cousin, economists. For full analysis, click here

An ominous prospect that policymakers already considered in July is that both weak growth and persistent consumer-price gains could set in — otherwise known as stagflation.

Whatever the outcome on Thursday, it’s likely that President Christine Lagarde will want to drive home a message that the ECB won’t let inflation keep a firm foothold, perhaps meaning that rates will need to stay high to make sure their job gets done.

Elsewhere, a crucial consumer-price report in the US will be watched by investors and policymakers, China releases key industrial data, and labor market numbers in the UK will inform the Bank of England’s upcoming rate decision.

Click here for what happened last week and below is our wrap of what’s coming up in the global economy.

US and Canada

Federal Reserve officials, who are observing a blackout period ahead of their Sept. 19-20 policy meeting, will digest another dose of key inflation data. On Wednesday, the government issues its consumer price index for August, followed a day later by a gauge of producer prices.

The core CPI, which excludes food and energy, is seen showing a third-straight 0.2% monthly rise. Compared with August of last year, this key measure of underlying inflation probably rose by 4.3%, the smallest annual advance since September 2021.

Such prints would be consistent with expectations Fed policymakers will keep interest rates on hold at their upcoming meeting. While underlying inflation cools, Wednesday’s report is also projected to show that overall CPI accelerated from a month earlier as gasoline prices turned higher.

In addition to the price data, retail sales figures are expected to indicate consumer demand wavered in August after registering solid advances in recent months. Other US economic reports include August industrial production and September consumer sentiment.

Meanwhile, in Canada, home sales data for August will show whether the market is continuing to cool, even as high prices remain detached from local incomes.

Canadian economic data releases also include wholesale trade, international securities transactions and manufacturing sales for July.

- For more, read Bloomberg Economics’ full Week Ahead for the US

Asia

A slew of figures from China will likely grab the most attention among economic data releases in Asia.

Industrial output and retail sales due Friday are both expected to have edged up in August, potentially offering an early signal that the world’s second-largest economy may be over the worst.

Malaysia releases factory output on Monday followed by business and consumer confidence surveys in Australia on Tuesday. Indian inflation is seen slowing and its factory output strengthening in figures out later that day.

Minutes from the Bank of Korea’s August meeting will likely show further support for its extended hawkish hold. Unemployment figures come out Wednesday from South Korea and the next day from Australia.

Thursday morning in Asia will also see the reaction to overnight inflation figures out of the US ripple through a range of asset classes.

Policymakers in Tokyo will likely be on edge to see the impact on a yen hovering around year-to-date lows against the dollar.

- For more, read Bloomberg Economics’ full Week Ahead for Asia

Europe, Middle East, Africa

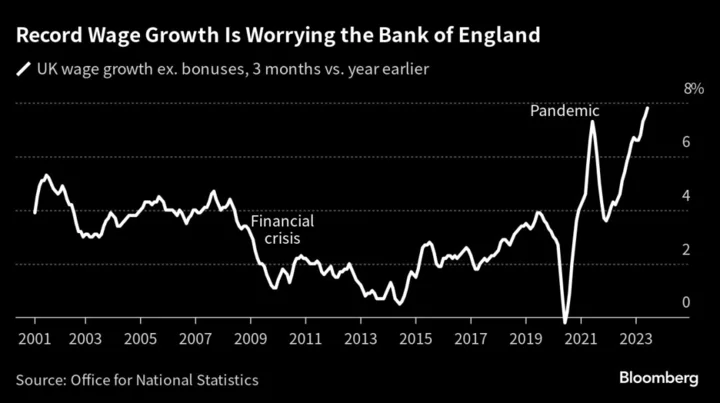

The UK may deliver some of the most watched economic data of the week as labor-market numbers potentially offer mixed signals for policymakers, with the prospect both of a higher unemployment outcome and still-robust wage growth.

Also useful for officials due to set rates the following week will be gross domestic product numbers for July, signaling if the economy’s somewhat surprising resilience lasted into the third quarter. Forecasters anticipate a decline from June.

While the ECB decision will take center stage in the euro region, the release of European Commission forecasts on Monday may offer investors an initial taste of how officials in Brussels view the immediate outlook for growth and inflation.

Inflation data is on tap across the Nordics. Both Denmark and Norway release such numbers on Monday. Sweden’s report on Thursday is seen showing a marked slowing — though that may not be enough to stop the Riksbank from hiking rates again the following week.

Four other central bank decisions across Europe and Africa will keep investors busy:

- In Ukraine on Thursday, the central bank is likely to continue monetary policy easing after a bigger-than-estimated cut in July.

- In Russia, officials on Friday will hold the first scheduled meeting after an emergency August hike of 350 basis points to stem the ruble’s depreciation. Another increase is feasible after currency weakness.

- The same day in Angola, the central bank faces a close call between a hold or a hike to tame soaring inflation.

- Also on Friday, slowing inflation in Mauritius and less volatility in external balances may persuade rate setters to hold borrowing costs again.

Over to the Middle East, and on Sunday, Egypt releases inflation data for August. Investors will be watching to see if price growth accelerated beyond July’s figure of 37% or whether the central bank’s surprise hike in early August helped it to slow.

In Turkey on Monday, data will likely show a trade deficit in July, following a rare and small surplus a month earlier.

And Israel’s inflation probably accelerated to 4% last month. The data, out on Friday, may increase pressure on the central bank to resume hiking rates.

- For more, read Bloomberg Economics’ full Week Ahead for EMEA

Latin America

Argentina’s central bank estimates that last month’s peso devaluation may have fueled a 10.6% jump in monthly inflation, the fastest since the economy was coming out of hyperinflation more than three decades ago.

Local economists see the data out this week showing a monthly rise of as much as 13%.

Colombia’s economy has slowed to a crawl in 2023 after two years of torrid growth. July manufacturing, industrial output and retail sales data should all post negative prints for a fifth straight month.

In contrast, analysts are marking up their forecasts for Mexico’s economy. Expect industrial production data for July to come in above trend and possibly beat estimates for the seventh time in nine months.

In Peru, look for the central bank to keep its key rate at 7.75% for one more meeting due to stubbornly elevated inflation. The economy fell into a technical recession in the first half and the July GDP-proxy reading out Friday may offer more of the same.

Brazil data should underscore the challenges confronting Latin America’s central bankers: analysts expect that inflation accelerated for a second month in August, printing just below 4.7%.

Regionally, the direction of travel, while quite clear, is also proving painfully slow.

- For more, read Bloomberg Economics’ full Week Ahead for Latin America

--With assistance from Vince Golle, Robert Jameson, Zoe Schneeweiss, Laura Dhillon Kane, Monique Vanek, Greg Sullivan, Paul Wallace, Patrick Donahue, Paul Jackson and Andrew Langley.