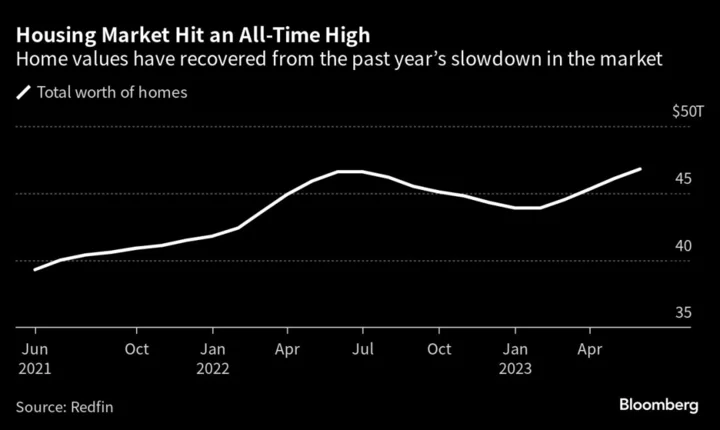

The US housing market has regained the nearly $3 trillion in value that was wiped out during the past year’s slowdown, according to an estimate from brokerage Redfin Corp.

A shortage of listings has pushed up prices, boosting the total value of US homes to a record $47 trillion, the brokerage reported.

Many homeowners locked in cheaper mortgage rates before borrowing costs started surging last year, leaving them reluctant to give up those loans. Just 1% of US homes changed ownership this year, the lowest share in at least a decade, according to Redfin.

The owners are “staying put because moving would mean taking on a rate that’s twice as high,” Chen Zhao, Redfin Economics research lead, said in the report. “This means buyers who are in the market now are duking it out for a very small pool of homes, preventing home values from plunging.”

Atlanta’s homes had the biggest jump in value, rising $40.1 billion from last June. Boston posted a $33.4 billion gain, while values in Miami were up $30.3 billion.

On a percentage basis, the largest gains were in relatively affordable markets. Little Rock, Arkansas, homes saw an 8.8% gain from a year earlier, where values in Camden, New Jersey, rose 8.7%. The more-reasonable set of costs in those cities likely bolstered buyer demand, according to Redfin.

Read More: Homeowners in US Who Want to Move Can’t Find Anything to Buy

Values fell from a year earlier in 32 metropolitan areas, and California cities were among the hardest hit. Los Angeles had the largest decline — nearly $153 billion — followed by Oakland, with almost $86 billion. San Francisco home values decreased about $58 billion.