An upgrade of Ford Motor Co.’s credit rating to investment grade is signaling a shift in corporate priorities as companies shore up their finances in the face of a potential recession.

The US automaker this week clinched a blue-chip grade from S&P Global Ratings, a move that lifts Ford’s debt out of junk and stands to shrink a global benchmark of high-yield bonds by $46.8 billion, the most since the mid-2000s. To some on Wall Street, that’s just the beginning.

“There’s still more to come,” said Matt Brill, head of North America investment-grade credit at Invesco Ltd. “We’re more likely to see improving credit fundamentals, even as the economy slows — rather than the opposite, which is what a lot of people are concerned about.”

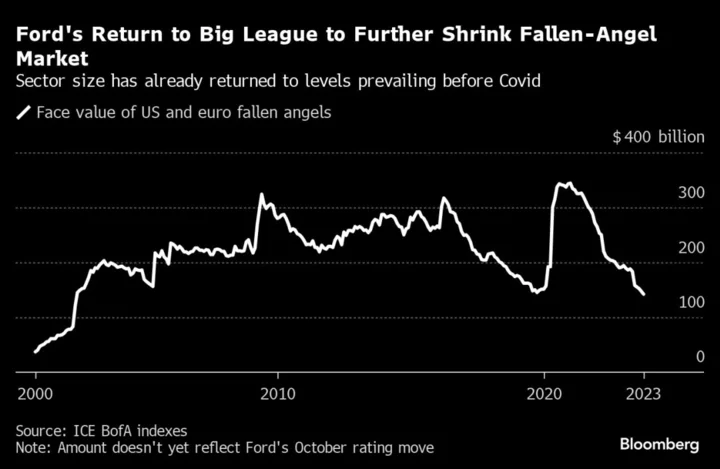

That’s a complete turnaround from early in the pandemic, when credit assessors delivered the most brutal wave of corporate-debt downgrades on record. Already, credit upgrades this year have decreased the amount of so-called fallen-angel bonds — or debt that was cut from investment-grade to junk — to $142 billion from as much as $344 billion in 2020, according to ICE BofA index data analyzed by Bloomberg.

And even as the focus settles on the risk of a recession as major central banks keep interest rates elevated, strategists at Bank of America led by Yuri Seliger see few indications that the number of fallen angels will rise again. Less than 0.5% of the investment-grade universe trades at spreads wider than their junk-rated peers, they wrote in a note earlier this month.

“The fallen angel pipeline seems to be quite thin,” unlike in previous economic cycles, said Maria Staeheli, a senior portfolio manager at Fisch Asset Management. “This time around, it feels like more companies are able and willing to take credit friendly action to keep IG ratings.”

Barclays Plc strategists led by Bradford Elliott, in fact, expect $70 billion to $90 billion of debt to be lifted from junk to investment grade — a type of upgrade that dubs the debt as rising stars — in 2024. Coty Inc., Cellnex Telecom SA and British retailer Marks & Spencer Plc are all in line for potential rising-star upgrades, according to the firm.

Representatives for Coty, Cellnex and Marks & Spencer didn’t respond to requests for comment.

The strategists, meanwhile, see only $20 billion to $40 billion of debt going from a high-grade score to high-yield next year. Others, though, are still bracing for pockets of weakness.

The increase in positive rating activity comes ahead of what’s expected to be a much more difficult time, Bloomberg Intelligence analyst Joel Levington said in an interview Tuesday. Still, bond graders are betting there’s enough cushion in their ratings to absorb downside, he said, adding that “there’s a lot of questioning of that logic.”

In Europe, Barclays strategists including Craig Nicol expect a net €15 billion ($15.9 billion) of fallen angels in 2024 as the “inexorable rise in interest costs as debt is refinanced will put incremental pressure on finances.”

Rising Star Boost

Rising star upgrades come with a clear set of benefits. S&P raised Ford’s rating to BBB- from BB+ on Monday, with a stable outlook. After this week’s move, Ford will be able to to borrow debt at lower rates and access deeper pools of capital, making it easier to fund operations.

The difference between yields on BBB rated debt — the lowest tier of investment grade — and BB rated debt, the highest-quality junk, is about 1.46 percentage points, according to data compiled by Bloomberg.

The upgrade will also yank Ford’s bonds out of fallen-angel and junk indexes. The carmaker accounts for almost a fifth of ICE BofA’s dollar-denominated fallen angel index, making it by far its largest component. It is also one of the largest pieces of the euro-denominated gauge, with a weight of more than 4%.

The fallen angels indexes will only reflect the change at the end of November due to rules on cutoff dates, according to a representative for the Intercontinental Exchange, Inc., which publishes the indexes.

And Ford is only the latest example. Occidental Petroleum Corp., which was another fallen angel in pandemic downgrade cycle, shed its junk status in May after an upgrade from Fitch. The promotion followed a similar move by Moody’s in March. Packaged-food maker Kraft Heinz Co. also climbed out of junk status after a second upgrade from junk.

Representatives for Ford, Occidental and Kraft didn’t respond to requests for comment.

“During this cycle — and coming from the pandemic — companies haven’t had time to lever up,” said Shanawaz Bhimji, head of corporate bond research at ABN Amro Bank NV. “We basically have a limited environment for fallen angels.”

(Updates with detail on Ford’s rating change in 12th paragraph. An earlier version corrected a reference to the rating move in chart note.)