Key economic data this week may suggest China’s recovery is doing a lot better than it is in reality.

Official figures on Tuesday are expected to show rapid year-on-year growth in industrial output and retail sales for April, with both of those key datasets likely accelerating from March. Fixed-asset investment through the first four months of 2023 is also projected to have gathered pace.

The figures come with a major caveat: they all compare to an extraordinary time period in China last year, when the manufacturing and finance hub Shanghai was locked because of spreading Covid cases, and restrictions on movement slowed or halted activity elsewhere.

That means that while economists usually pay close attention to year-over-year data in China, this time they may view month-on-month comparisons as a better indicator.

Recent figures have provided evidence that the economy’s momentum — which had so far been driven by the release of pent-up demand — is cooling. China’s consumer prices barely grew last month, while new borrowing slumped and housing market sales are starting to fizzle. April trade data showed imports plunging and export growth slowing down as well.

The lopsided recovery has raised questions about how much the world’s second-largest economy can boost global growth this year, when other nations had hoped the end of China’s pandemic restrictions would benefit their own exports.

What Bloomberg Economics Says:

“China’s April activity data will probably offer another instance of headline figures that can’t be taken at face value. We expect production and retail sales to jump — by comparison with last year’s terrible numbers, which cratered during Shanghai’s lockdowns.”

—Chang Shu and David Qu, economists. For the full report, click here

It’s also fueling debate about whether the People’s Bank of China will ease monetary policy. Some economists argue the central bank has scope to act this year — including cutting its benchmark policy rate — now that the US Federal Reserve seems likely to pause hiking.

Bloomberg Economics, bucking consensus, expects a rate cut to come immediately as growth “clearly needs support.” Others say the country should prioritize measures that bolster business confidence and ensure household income growth, given how ample liquidity is now.

Elsewhere, Japan will release inflation and growth numbers, the European Commission will publish new quarterly economic forecasts, Mexico’s central bank has a cliffhanger rate decision, and data in the US are likely to show more economic weakness.

Click here for what happened last week and below is our wrap of what is coming up in the global economy.

Asia

There’s plenty else on the agenda aside from the Chinese data.

In Thailand, gross domestic product data on Monday — a day after that nation’s election — will likely show a pickup in growth, while the Philippine central bank may pause its rate-hiking cycle on Thursday.

India releases trade figures on Monday, while New Zealand and Malaysia will publish theirs on Friday.

Japan will also report on its first quarter GDP figures on Wednesday, likely eking out further growth, while inflation is expected to show a further acceleration on Friday, sharpening the cost-of-living impact.

- For more, read Bloomberg Economics’ full Week Ahead for Asia

US Economy and Canada

The US calendar offers glimpses into consumer demand, the housing market and manufacturing at the start of the second quarter. Government data on Tuesday are projected to show a rebound in April retail sales, fueled largely by stronger results at auto dealers.

The same day, figures from the Fed are likely to show a modest increase in April factory output after the biggest slide in three months. Outside of a steady appetite for motor vehicles, many producers are struggling with softer demand for merchandise.

Among housing-related data for April, beginning home construction and sales of previously owned homes are projected to drop as the sector continues to struggle for momentum in a higher interest-rate environment.

The calendar for Fed officials is busy, and includes two days of congressional testimony from Vice Chair for Supervision Michael Barr on current stress on the banking system and the central bank’s response. At the end of the week, Fed Chair Jerome Powell joins former Chair Ben Bernanke in a panel discussion at a monetary policy research conference.

Other Fed officials scheduled to speak include board members Philip Jefferson and Michelle Bowman, and regional bank presidents Lorie Logan, Loretta Mester and Austan Goolsbee.

Further north, a fresh batch of inflation data will inform trader bets on the future path of rates, and the Bank of Canada will release its annual review of the financial system amid renewed global banking concerns.

- For more, read Bloomberg Economics’ full Week Ahead for the US

Europe, Middle East, Africa

A week interrupted in some continental European countries by a holiday on Thursday will be bookended by two major economic assessments.

On Monday, the European Commission will reveal quarterly forecasts with a fuller look than February’s edition that includes projected debt and deficits.

Officials said last time that the euro-zone economy will fare better than previously feared. They’ll need to balance that against weak German data and evidence of mounting global headwinds. Their inflation outlook may also draw interest as price growth shows few signs of slowing.

On Friday, after the market close, Moody’s Investors Service will say if its negative outlook on Italy should transform to a downgrade, marking the country’s first junk rating.

Read more: Italy Survives Fitch Judgment in Boost for Meloni Before Moody’s

It’s a quieter week for data, with industrial production for March on Monday, and second readings of GDP and inflation due on subsequent days.

Several European Central Bank officials will speak, just as they increasingly acknowledge their tightening cycle may not be on the verge of ending. President Christine Lagarde delivers comments on Friday, and other public appearances include Executive Board members Luis de Guindos and Isabel Schnabel and central-bank chiefs from Germany, Ireland and Spain.

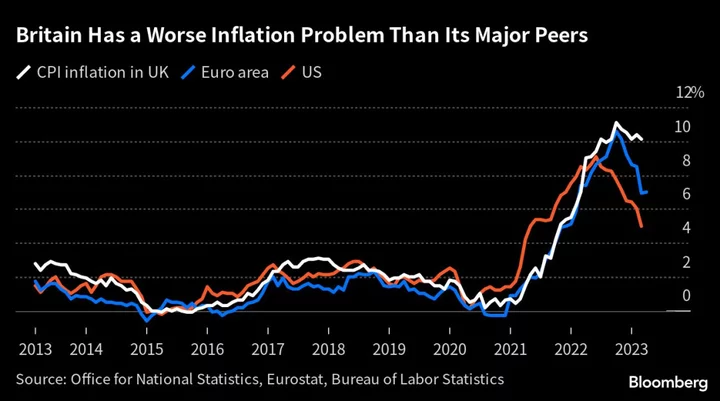

In the UK, where the Bank of England just raised rates and signaled further tightening, wage data on Tuesday will be closely watched. Governor Andrew Bailey and several other officials will make public appearances before lawmakers or at other events.

In Sweden, inflation data for April on Monday will draw attention after a recent hawkishly tilted decision by the Riksbank, just as the housing market’s woes hurt economic growth.

Multiple GDP reports from around Europe are scheduled, from Denmark to Slovenia to Poland. Perhaps most interesting will be Hungary’s, due on Tuesday; its economy probably contracted in the first quarter amid a deepening recession and the fastest inflation and highest interest rates in the EU.

Three central-bank decisions are due across the African continent:

- The Bank of Zambia will likely raise its key rate on Wednesday for a second time this year to contain double-digit inflation and support its currency, which has come under pressure from slow progress in debt-restructuring talks.

- A temporary slowdown in price growth may give Egypt’s central bank room to pause its monetary tightening on Thursday.

- On Friday, Angolan policymakers will probably cut borrowing costs for a third time this year as inflation continues to cool. Governor Jose de Lima Massano said last month that if price pressures ease further, “we will probably be ending the year with the basic interest rate around 15%.” The rate currently stands at 17%.

Finally, the outcome of Turkey’s close-run election will be a major focus of investors.

- For more, read Bloomberg Economics’ full Week Ahead for EMEA

Latin America

On a busy Monday, Brazil’s much-watched Focus survey, Peruvian economic activity and Lima labor market data lead off ahead of Colombia’s first-quarter output report. After expanding 11% and 7.5% in 2021 and 2022, economists surveyed by Bloomberg expect growth of just 1.1% for 2023 and 2.2% for 2024.

Chile’s economy likely expanded for a second straight quarter in the three months through March. Its finance ministry now sees a 0.3% expansion this year compared to a previous estimate of a 0.7% decline.

On Tuesday, Uruguay’s central bank may follow April’s surprise quarter-point rate cut with another move down as a multi-year drought batters the economy.

In Brazil, the rapid cooling in inflation and government household support may have kept retail sales buoyant in March while GDP-proxy data for the same month is more than likely to come off February’s near three-year high.

Banxico’s meeting is tough to call: after 15 hikes and 725 basis points of tightening over 23 months, there’s a real chance the central bank is done. Will board members led by Governor Victoria Rodriguez Ceja call it a day at the current 11.25%, or go for one more quarter-point increase to take the key rate to 11.5%?

- For more, read Bloomberg Economics’ full Week Ahead for Latin America

--With assistance from Vince Golle, Sylvia Westall, Andrea Dudik, Nasreen Seria, Jill Disis, Fran Wang, Robert Jameson and Laura Dhillon Kane.