The zero-day options trade that has taken Wall Street by storm will finally arrive in Europe next week, in a fresh test for the region’s long-struggling capital markets.

Starting Monday, Deutsche Boerse AG’s Eurex will list Euro Stoxx 50 (SX5E) derivatives that expire every weekday, following US peers who introduced the now-booming contracts tied to the S&P 500 last year. Every trading session, investors in Europe will be able to buy and sell derivatives expiring the same day, known as zero-days-to-expiration contracts, or 0DTE.

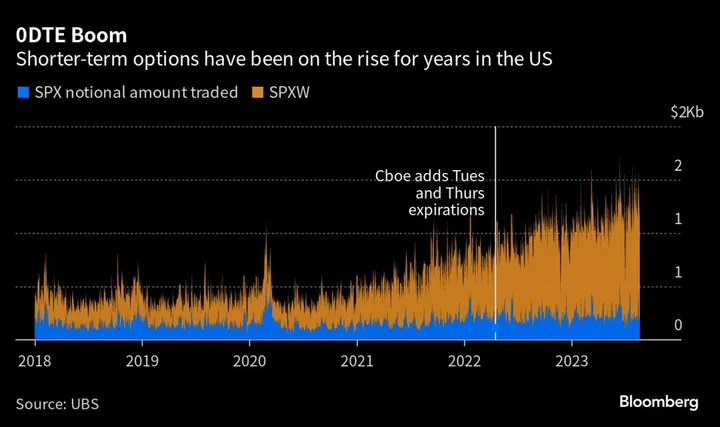

Their introduction unleashed a torrent of trading activity on the other side of the Atlantic, as retail and institutional investors used them as a tool for speculation and hedging.

At one point this month 0DTE accounted for a record 55% of the trading volume for options tied to the S&P 500, according to data compiled by Nomura Securities International. The derivatives have grown so popular that some now fear they’re swaying America’s benchmark equity gauge itself.

In Europe, the level of demand for the contracts will be closely watched by participants looking for signs of life in the moribund market. But amid the chronic underperformance of equity benchmarks, dwindling stock listings and stagnant volumes, the options face an uphill battle to have an impact.

“You don’t have that same kind of pent-up demand,” said Kieran Diamond, a London-based derivatives strategist at UBS Group AG. “And the S&P just has a very strong track record as the main global liquidity pool for equity volatility.”

As of Tuesday, the daily notional amount of Euro Stoxx 50 options traded averaged $45 billion over the past month, data compiled by UBS show. For the US benchmark, the equivalent figure was nearly $1.3 trillion.

Even before the addition of Tuesday and Thursday expirations last year — which made it possible to trade S&P 500 products expiring every weekday — weekly options had been growing in popularity in the US, Diamond noted. In contrast, activity in options tied to the SX5E is mainly focused on monthly contracts.

While the new expirations are unlikely to generate a frenzy to match the US, they may still lift volumes, with trading pros as the main users, according to Patrick Bonouvrie, head of European index derivatives trading at Optiver BV.

“There’s been a clear trend globally in investors showing greater preference for shorter-dated options,” Bonouvrie said by email. “Daily options allow for the hedging of very specific risks – such as ECB events – that couldn’t be hedged with the same granularity before.”

Eurex has previously said the new contracts are a response to increasingly strong demand from institutions for more options with short-term expiries. Alongside the introduction of daily expirations, the derivatives will also now settle at the stock-market close of 5:30 p.m. Central European Time, instead of the current midday settlement. That will allow greater scope to trade events during the market day.

The new derivatives are unlikely to find much retail investor interest, however. Day traders have turned out to be a notable driver of the 0DTE boom in the US, the exchange at the center of the frenzy said this week. But retail participation overall in the equity market in Europe is substantially lower than across the Atlantic, suggesting a key source of demand simply isn’t present.

To some, that may be no bad thing. Strategists in the US have speculated that 0DTE activity is now so large it can move the S&P 500, as option dealers rush to hedge their own positions while traders furiously buy and sell contracts in response to intraday swings.

It’s all the subject of a heated debate with no end in sight — one that Europe is unlikely to be part of any time soon.