The US consumer is starting to buckle as rising gas prices crimp spending and the delinquency rate on credit cards reaches the highest level in more than a decade. And that’s before student loan payments restart in October.

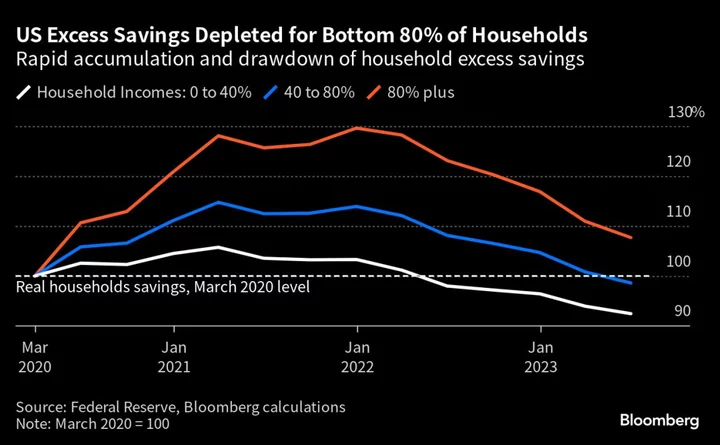

A measure of consumer confidence slumped to a four-month low in September as inflation and a deteriorating outlook for the economy weigh on people. That’s a blow given that individual spending fuels about two-thirds of the US economy, and the vast majority of Americans now have less savings than they had before the pandemic after adjusting for inflation.

“Consumer debt quality is declining, signaling potential risks in certain credit market areas,” Moody’s Investors Service said in a report this week. In addition, “many consumer product companies were highly leveraged following a debt splurge in recent years, leaving them vulnerable.”

For companies with heavy debt loads, pressure on consumers can translate to credit trouble. Investors including Blackstone Inc.’s Mike Carruthers say there will be a split between companies that can grow fast enough to keep up with rising borrowing costs and those that can’t.

High-yield retailers are among those potentially hobbled by sales and profitability pressures that put them at increasing risk of downgrades, according to Bloomberg Intelligence credit analyst Mike Campellone.

Household purchasing power has already fallen, Hennes & Mauritz AB Chief Executive Officer Helena Helmersson told analysts this week, with large retailers such as Target Corp. seeing a drop in discretionary spending.

“There is some real concern about weakness in the consumer,” Sarah Hunt, a partner at Alpine Saxon Woods, said in an interview with Bloomberg TV this week. Higher gas prices, in particular, mean “there’s a real spending issue coming up and I think that’s going to impact earnings.”

Until now, consumers have been fairly resilient, buoyed by a strong labor market. But weaknesses are emerging among young people and lower-income households. That helped send the 60-day-plus delinquency rate for subprime auto loans in July to the highest-ever level, S&P Global Ratings said in a note this month.

“It’s not a crisis at this point, but clearly the delinquency rates are rising and they’re doing so at a time where unemployment remains relatively low,” said Cristian DeRitis, deputy chief economist at Moody’s Analytics. A modest increase in jobless numbers is “going to just put more pressure” on those rates.

It’s part of a wider realization among market participants that we may be in for a long, drawn-out default cycle as the impact of higher borrowing costs slowly works its way through the system.

Citigroup Inc. credit strategists including Michael Anderson wrote in a note this week that they expect high-yield and loan default rates to reach 4.6% and 5.3% by the third quarter of next year, up from 3.2% and 4.9% respectively.

“We anticipate stubbornly high rates as tighter monetary policy and expansive fiscal policy” combine “to form a tough environment in which to refinance the substantial maturity wall coming due in the coming year,” they wrote.

Week in Review

- Almost two years after China’s Evergrande defaulted on its debt, its billionaire founder and chairman, Hui Ka Yan, is under police control on suspicion of committing unspecified crimes.

- Meanwhile, the company’s mainland unit said it failed to repay an onshore bond, adding a new layer of uncertainty to the developer’s future as a restructuring plan with its offshore creditors teeters.

- Companies that need to refinance hundreds of billions of dollars of floating-rate loans stemming from the cheap-money era are increasingly tapping private credit funds for high-cost debt that lets them delay interest payments.

- BlackRock Inc. said insurance executives overseeing $29 trillion plan to pour more money into private debt and credit strategies while cutting back on private equity and real estate.

- Investment banks and direct-lending funds are competing to provide as much as €4 billion ($4.2 billion) of debt to finance a potential take-private of European classifieds company Adevinta ASA.

- Direct-lending funds are working to provide as much as £1.25 billion ($1.5 billion) for the potential buyout of the UK’s Iris Software.

- Bankers and private credit funds are working on a financing deal of around €1 billion ($1.05 billion) to back a potential buyout of French insurance broker Kereis as the sale process kicks off.

- Blackstone Inc. is looking to raise over $10 billion across two private loan funds in Europe and the US.

- Private credit lender Värde Partners has raised around $1.5 billion to invest in asset-based lending.

- Wells Fargo & Co. and Centerbridge Partners are joining forces on a direct-lending fund.

- Private credit funds with more than $5 billion under management took the largest share of capital raised by the asset class in the first half of 2023, according to PitchBook.

On the Move

- Banco Santander SA has hired Credit Suisse Group AG veteran Joel Kent as head of leveraged finance trading.

- Arrow Global Group Ltd has recruited Toni McDermott as chief investment officer of credit and direct lending, and Zachary Vaughan as head of real estate.

- Rather than hiring bankers with experience in private credit and high salaries, Sumitomo Life is sending existing staff to the US to get multi-year training in the booming alternative asset area.

- Sherwood Partners has launched an advisory unit focused on restructurings and turnarounds of middle-market companies.

--With assistance from Dan Wilchins.