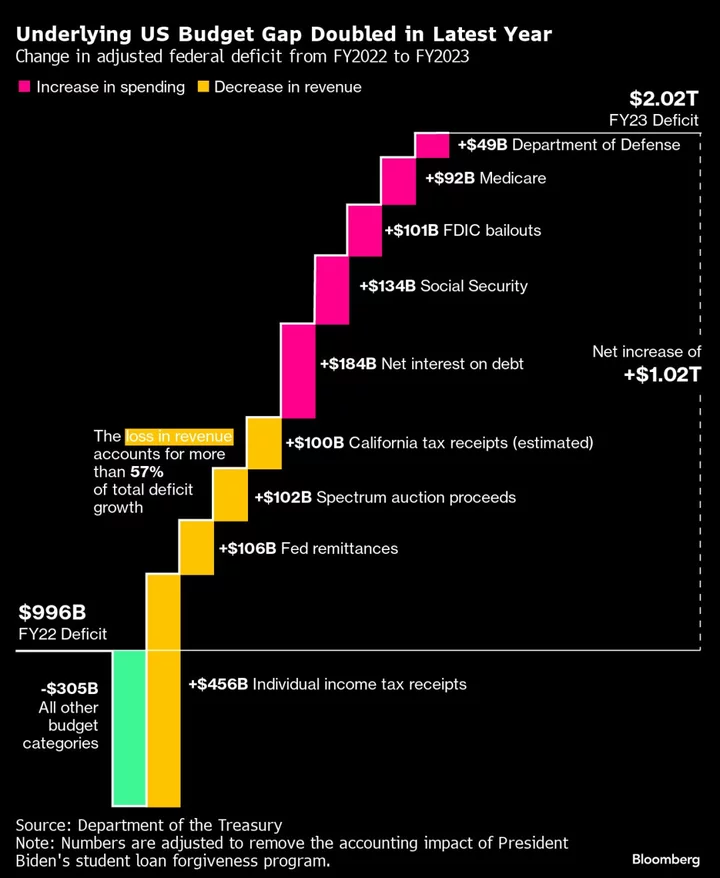

In a year when the US economy exceeded almost everybody’s expectations, the underlying federal deficit roughly doubled, spotlighting a dire fiscal trajectory likely to only worsen the partisan budget battles in Washington.

The government ran a $2.02 trillion deficit for the fiscal year through September, after adjustments to remove the impact of President Joe Biden’s student-loan forgiveness program, which was scotched by the Supreme Court. The gap is $1.02 trillion more than the prior year.

The surge is a powerful illustration of a fiscal path that’s triggered warnings from economists, politicians and credit rating agencies. It also helps explain why yields on longer-term US Treasuries are reaching highs unseen since before the global financial crisis, with the government needing to issue ever more debt to cover the shortfall of revenues relative to spending. Ten-year yields surpassed 5% on Monday.

Republican lawmakers have blamed Biden for out-of-control spending, though have been so at odds over how to address the budget that they’ve struggled to unite over a new speaker of the House. Meantime, spending needs continue to rise, with the White House calling for $106 billion in emergency funding for Israel, Ukraine and the US-Mexico border.

For all the politicking about spending, however, the main cause of the widening in the deficit in 2023 is actually on the revenue side. Much of the rest is due to the knock-on effects of faster inflation, a dynamic that’s also subject to bitter partisan debate.

Measured as a share of gross domestic product, the adjusted widening in the deficit marks one of the three worst years since 1950, according to JPMorgan Chase & Co. The other two came during times of crisis: 2009 and 2020. But the 2023 fiscal year saw strong economic growth, with more than 3 million people added to US payrolls.

The following are the main drivers of the widening:

Accounting Adjustments

The figures above remove the impact of the Biden administration’s student-loan forgiveness program. That had increased the 2022 deficit by $379 billion, but after the move was struck down by the Supreme Court, the Treasury had to reverse most of the accounting by reducing the 2023 shortfall by $320 billion.

Most fiscal watchers have taken out the student-debt numbers from 2022 and 2023 to get a clearer look at the federal budget.

Individual Taxes

There was a $456 billion plunge in individual income-tax receipts, the single largest shift in flows over the two years.

Part of that was thanks to a major reversal in financial markets from 2021 to 2022. In 2021, the S&P 500 Index of US stocks rose about 27%, while bonds and other assets also appreciated — boosting taxes on realized gains. But in 2022, the S&P 500 dropped 19%, with bonds also plunging — walloping revenue from capital gains and other investment earnings owed this year.

Tax receipts took another hit due to filing extensions granted to households and businesses in areas affected by disasters. That notably included almost all of California, pushing revenue from the Golden State, estimated by the Bipartisan Policy Center at about $100 billion, out of fiscal 2023 and into fiscal 2024.

Bidenomics Packages

The impact here was marginal. The $1.9 trillion Covid-relief bill of 2021, known as the American Rescue Plan, has largely come and gone. The other three signature pieces of legislation — the bipartisan Infrastructure Investment and Jobs Act, the CHIPS and Science Act, which subsidizes semiconductor manufacturing, and the Inflation Reduction Act — aren’t yet hitting the budget with force.

Inflation and Entitlements

Federal benefits paid in 2023 received a cost-of-living adjustment of 8.7%, reflecting the surge in inflation that peaked in 2022. Social Security accounted for $134 billion of the deficit increase, and Medicare another $92 billion.

Inflation and the Fed

The Federal Reserve used to pass along a large amount of cash to the Treasury thanks to the interest it earned on its large bond portfolio. But that’s over now that the Fed is paying out a lot of interest on the cash that commercial banks park with it. That deposit rate used to be near zero, but is now well over 5%. And that’s a much higher a rate than the payout of the average bond in the Fed’s portfolio.

This dynamic contributed $106 billion to the increase in the federal government’s deficit.

Inflation and Bonds

The Fed’s rate increases of course have also driven up yields on the federal debt that the Treasury issues. The weighted average rate the Treasury pays on marketable securities has climbed to more than 3%, the highest since 2009. In all, net interest costs on debt added $184 billion to the deficit this year, a Treasury official told reporters last week.

The Rest

Other categories that contributed to the increase include defense spending, payouts from the Federal Deposit Insurance Corp. to bail out customers of failed banks and a drop in revenue from the auction of licenses to use the electromagnetic spectrum.

The Future

The deficit for the fiscal year that began Oct. 1 will likely shrink, thanks in part to the positive performance of financial markets in the 2023 calendar year — which ought to boost revenues when taxes are paid in 2024. The delayed California receipts will also help.

But the Fed still won’t likely be paying the Treasury, and the Treasury is going to be paying higher and higher interest on its debt for some time. That’s created a vicious cycle, because the higher interest costs only add to the deficit, requiring more debt to be sold.

“What we’re really seeing is that $2 trillion is the new normal for deficits,” said Marc Goldwein, senior policy director at the Committee for a Responsible Federal Budget, a fiscal watchdog.

It sets up a political battle when major elements of former President Donald Trump’s tax cut package expire at the end of 2025. The Biden administration has already begun floating a narrative that those reductions are part of the reason for the deficit widening.

The Republican candidates for president are calling for more tax cuts to lift growth rates, arguing that will also boost revenues in time.

Meantime, look for wider deficits in updated long-term projections from the Congressional Budget Office and White House Office of Management and Budget in the spring, to account for the new dynamic of higher borrowing costs.

--With assistance from Jennah Haque, Chloe Whiteaker, Viktoria Dendrinou and Kathleen Seaman.