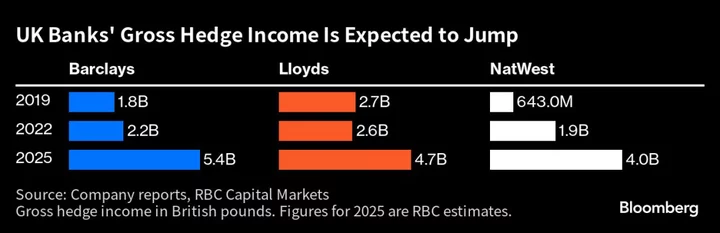

The UK’s biggest banks stand to gain billions this year from hedging against rising rates.

Structural hedges, the balance sheet exercise which reduces banks’ sensitivity to interest rate moves, were worth well over £1 billion ($1.3 billion) at each of Britain’s top lenders in the first half of 2023. At Barclays Plc, hedging income for 2023 is expected to surge more than 60% to £3.6 billion.

Finance chiefs this quarter confirmed that the hedge, which could also be described as a bank’s fixed-income portfolio, will be a major contributor to earnings as swap contracts reprice at higher interest rates. This trend is widely expected to help lenders offset income hits from tougher mortgage competition and pressure to pass on a greater share of rate hikes to customers.

As swap contracts mature, “we do expect through to 2025 that the uplift from the hedge activity remains sizable,” NatWest Group Plc Chief Financial Officer Katie Murray said on the bank’s analyst call last week.

This year’s collapse of US regional lenders including Silicon Valley Bank has underscored the importance of lenders’ asset and liability management, which can come under particular pressure when depositors withdraw huge sums or switch to higher-yielding savings accounts.

Lenders therefore buy financial derivatives with the effect that rate moves don’t impact interest income as fast as they would without a hedge.

“The reason that we have the structural hedge is to smooth the income of our banking book businesses over time,” Barclays Chief Financial Officer Anna Cross told analysts last week.

Ivory Towers

The hedge is implemented by treasury teams, one of whose main responsibilities is to secure banks’ wholesale funding. They have a reputation for being more academic than a typical trader.

“I’ve heard the term ‘ivory tower’ a couple of times in my career, seeing treasury as a place for technical discussions that feel disconnected with the rest of the bank,” said Justin Fox, group treasurer at Virgin Money UK Plc. “In reality treasury is a critical business partner to the commercial teams, helping balance risk and reward pricing strategies.”

The number of Treasury staff who work on the structural hedge can vary from 50 to 500, depending on the bank’s size, with asset and liability management analysts and execution teams mostly involved. Decisions on the hedge are also made at banks’ risk committees which typically include board members, the finance chief and chief executive.

Caterpillar or Dynamic

There are two main approaches.

The first one — called ‘caterpillar’ — doesn’t see a bank take a view on future interest rate moves, while the other, ‘dynamic’ approach is employed by banks that make calls on the market and time purchases of swap contracts accordingly. While Barclays and NatWest follow the ‘caterpillar’ approach, Lloyds Banking Group Plc’s treasurers are known for applying a ‘dynamic’ one.

One of the most profitable moves in British banking was overseen by Antonio Horta-Osorio, who was chief executive officer of Lloyds between 2011 and 2021. When Horta-Osorio took over at the then-partly state-owned lender, he repositioned Lloyds’ hedge which allowed the bank to earn billions from rightly predicting that rates would stay low for a longer period.

While shareholders are likely to welcome such a windfall, the fact that this income is reliant on calling the market correctly can also make investors uneasy.

Getting It Wrong

If treasurers’ predictions don’t work out, scrutiny can be intense. When Standard Chartered Plc lost nearly $100 million in a quarter last year, CEO Bill Winters had to tell analysts that the bank’s timing was wrong.

Virgin Money canceled its structural hedge program in 2020 when the Bank of England’s benchmark rate stood at 0.10%. At the time, the UK’s sixth-biggest lender assumed rates could only rise and boost income even quicker without the hedge.

The bank ended up reversing its decision a few months later, after policy makers pointed out that the BOE could also introduce negative rates if needed.

“Most banks’ approach to structural hedging is mechanical,” RBC analyst Benjamin Toms said. “For those that employ a more dynamic investment method, timing is key.”

--With assistance from Harry Wilson, Greg Ritchie, James Hirai and Katherine Griffiths.