Office prices in the US are due for a crash, and the commercial real estate market faces at least another nine months of declines, according to Bloomberg’s latest Markets Live Pulse survey.

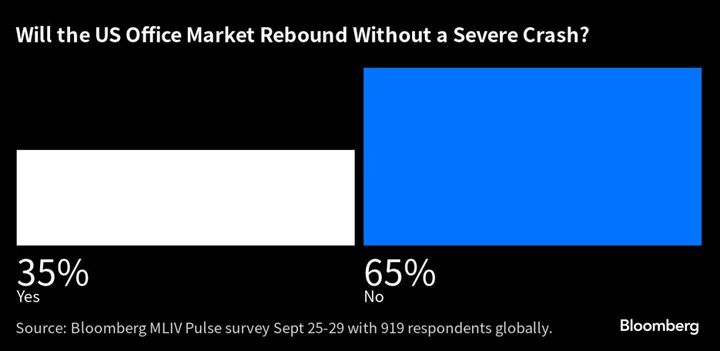

About two-thirds of the 919 respondents surveyed by Bloomberg believe that the US office market will only rebound after a severe collapse. An even greater majority says that US commercial real estate prices won’t hit bottom until the second half of 2024 or later.

That’s bad news for the $1.5 trillion of commercial real estate debt that according to Morgan Stanley is due before the end of 2025. Refinancing it won’t be easy, particularly the roughly 25% of commercial property that is office buildings. A Green Street index of commercial property prices has already fallen 16% from its peak in March 2022.

Commercial property values are getting hit hard by the Federal Reserve’s aggressive tightening campaign, which lifts a key cost of owning property — the expense of financing. But lenders looking to offload their exposure now are finding few palatable options, because there aren’t many buyers convinced the market is close to a bottom.

“Nobody wants to sell at a huge loss,” said Lea Overby, an analyst at Barclays Plc. “These are properties that don’t need to be sold for long periods of time, and that means holders are likely to delay a sale as long as they can.”

Adding to the trouble is stress among regional banks, which held about 30% of office building debt as of 2022, according to a March report from Goldman Sachs Group Inc. Smaller banks saw their deposits shrink by nearly 2% over the 12 months ended in August, according to the Fed, after Silicon Valley Bank and Signature Bank collapsed. That translates to less funding for the banks, giving them less capacity to lend.

Pain from higher interest rates can take years to filter through to owners of the US commercial real estate, which Morgan Stanley values at $11 trillion in total. Investors in office buildings, for example, often have long-term fixed-rate financing in place, and their tenants can be subject to long-term leases as well.

It will take until 2027 for leases that are in place today to roll over to lower revenue expectations, according to research by Moody’s Investors Service published in March. If current trends hold, then revenues by then will be 10% lower than today.

“It tends to be a slow reckoning for US real estate when rates change,” Barclays’s Overby said. “And the office sector is deeply distressed, which will take a long time to work out.”

Even if there is a serious and prolonged downturn in US commercial real estate, including major loan losses from a cratering office sector, Overby isn’t worried it will threaten overall market stability. The property sector is large, but the debt is spread across a wide enough array of investors to absorb losses, she said.

Besides high interest rates, offices are struggling with tenants cutting back or moving out, with the trend especially strong in the US, where office workers are more reluctant to badge in than in Europe or Asia. Some of the resistance to the return to offices could be attributed to commuting pains. More than 40% of MLIV Pulse respondents said they would be enticed to come to the office more often if they had better public transit options available.

About 20% of respondents said that they moved farther away from their office during the pandemic and only 3% regretted their escape. Nearly a third said their commutes got longer than before Covid, probably either because they moved, or because of pandemic-era transit service cuts.

The MLIV Pulse survey of Bloomberg News readers on the terminal and online is conducted weekly by Bloomberg’s Markets Live team, which also runs the MLIV blog. This week, the MLIV Pulse survey asks about quarterly earnings. Do you think retailers will warn about profits or surprise with positive outlooks? Share your views here.