A rare, relatively unknown technicality in the Treasury futures market stands to unleash fresh momentum in the selloff of US government bonds.

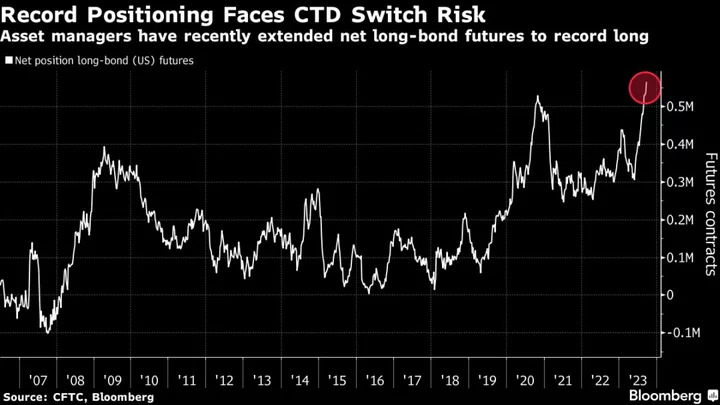

The fine print of futures contracts is coming into focus as Treasury yields surge, threatening to hit a market where investors have amassed a record sum of contracts. Barclays Plc strategists are already warning of what could potentially become the biggest futures-market disruption since 2015.

In Treasury futures, the contract terms dictate what type of securities are allowed to be delivered by traders with short positions to those with long positions. Market participants will typically identify the Treasury bond that is cheapest to deliver — or CTD — into futures, and the price on the related contract will follow the bond. But as cash Treasury yields soar, the CTD securities are at risk of quickly changing.

“It’s like a game of musical chairs. It’s all very calm and straightforward, until it’s not,” said David Robin, interest-rate strategist at TJM Institutional Services LLC. “Everybody’s walking around in a circle, then all of a sudden — chaos.”

A micro-sized CTD switch is already underway. The CTD for the December 2023 Treasury futures contract has switched to the 4.625% February 2040 bond — from the 4.5% August 2039 maturity.

There’s potential, however, for a wave of selling attached to CTD switches if Treasury yields keep marching higher.

A Bloomberg analysis shows a further yield rise of around 40 basis points could cause a bond maturing in 2042 or 2043 to become the new CTD, triggering futures selling by portfolio managers who must adjust for the duration shift on their futures positions.

“Dramatic moves in the marketplace create convexity shifts that have to be adjusted for,” TJM’s Robin said.

--With assistance from Elizabeth Stanton.