One of China’s largest developers is wobbling and has less than 30 days to avoid a default on its bonds, the latest signal of the government’s struggle to end the nation’s property slump as the economy slows.

Country Garden Holdings Co., which had total liabilities of 1.4 trillion yuan ($194 billion) at the end of last year, said it had underestimated the market downturn and is facing the biggest challenge since it was established in 1992. The property firm expects to post a net loss of up to 55 billion yuan for the first half of 2023 compared with earnings of about 1.91 billion yuan a year earlier.

Country Garden Real Estate Group Co Ltd. said it will suspend trading in nearly a dozen onshore bonds starting Monday, two days after the Chinese real estate company’s controlling shareholder said it would report a multi-billion-dollar loss for the first half of this year.

The developer’s liquidity crunch is adding to concerns about the potential drag the industry will have on growth in the world’s second-largest economy, sending a Bloomberg index of the country’s junk dollar bonds to the lowest level since last year on Thursday.

“What Country Garden messaged in the latest announcement just confirmed investors’ worst fears about the dire state of China’s ailing property market,” said Wee Liam Goh, a portfolio manager at UOB Asset Management.

Regulators across China’s government have been seeking since late last year to revive demand in the real estate sector, which makes up about a fifth of China’s gross domestic product. Measures such as easing mortgage rates on first-home purchases have so far failed to stem the crisis, with home sales tumbling the most in a year in July.

The downturn has left the property sector caught in a vicious cycle, after an earlier government campaign aimed at getting developers to deleverage caused housing purchases to slump. That crimped the cash flow of builders, leading to a record amount of defaults.

Unprecedented protests broke out across cities last year as builders ran out of cash to complete and deliver apartments to buyers, spurring policymakers to intervene. The Communist Party pledged further easing of property measures following its Politburo meeting in late July.

“While there have been positive policy signals” since then, “the property sector requires more tangible and timely policy support for stabilization,” said Andy Suen, co-head of Asia ex-Japan fixed income at PineBridge Investments. “Persistent defaults among developers could further dampen homebuyer confidence.”

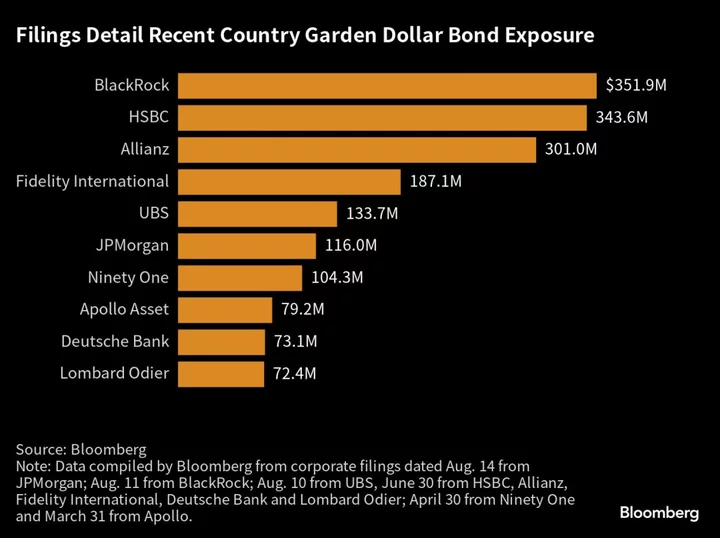

The latest crisis came after bondholders of two dollar notes issued by Country Garden, helmed by one of China’s richest women Yang Huiyan, failed to receive coupon payments due Aug. 7, according to bondholders who requested anonymity.

The renewed turmoil comes just as signs emerge that economic demand is weakening as hopes of a rapid recovery following the rollback of pandemic measures fizzle out.

Consumer and producer prices fell in July from a year ago, the latest data show. The statistics bureau said the contraction is likely to be temporary and consumer demand is improving.

Ultimately, “the economic recovery from the Covid reopening is mainly a consumption recovery, which makes it even more crucial to rescue the real estate sector at the current juncture,” said Tommy Wu, senior China economist at Commerzbank AG. “The failure of another major Chinese developer would pose tremendous pressure on the already-slowing economy.”

Week in Review

- Oaktree Capital Management is looking to raise more than $18 billion in what would be the largest-ever private credit fund.

- Private credit firms are raising billions of dollars to grab a share of the $5.2 trillion market that includes US consumer debt, seizing on a growth opportunity while the industry’s traditional lenders are in disarray.

- Financial technology consumer lender Oportun Financial Corp. has agreed to sell $700 million in personal loans to private firms, Castlelake LP and Neuberger Berman Group LLC.

- UBS O’Connor, the independent investment business within UBS Asset Management, plans to raise up to $2 billion for its third opportunistic private credit fund.

- Junk bonds are emerging as a sweet spot in global fixed-income markets as investors increasingly bet that major economies will avoid recession — for now.

- Yellow Corp. has drawn additional interest from potential financiers who are offering alternative bankruptcy financing for the short-haul trucking company that’s more affordable than a loan from lenders led by Apollo Global Management.

- Signs of stress are increasing for China’s local government financing vehicles, many of which are tasked with funding local infrastructure projects. Huaan Securities Co. said 48 LGFVs were overdue on commercial paper in July, versus 29 in June.

On the Move

- Cresset hired Bradley Schneider as managing director and head of private credit. He was previously head of private credit at Midwest Holding, and has more than 20 years of experience in private and alternative credit investing.

- Morgan Stanley credit trader Vladimir Strnad is leaving the bank after working there for seven years.

- Wells Fargo and Co. high-yield veterans Grant Jordan and Elliot Broadfoot left the bank this week.

- Joseph Otting, the former Comptroller of the Currency under Donald Trump, has joined Andalusian Credit Partners as a managing partner. The private credit firm debuted this year and is primarily owned by Jeffrey Kaplan and Nicholas Savasta.

- National Australia Bank has merged its loan originations and syndications teams and appointed Harry Staple to head the combined business. Stephen Boyd, who ran the private capital syndications team, is set to leave the bank in the middle of August.

- Sandeep Chandak is joining Hillhouse’s private credit business from Varde Partners. He will be a managing director.