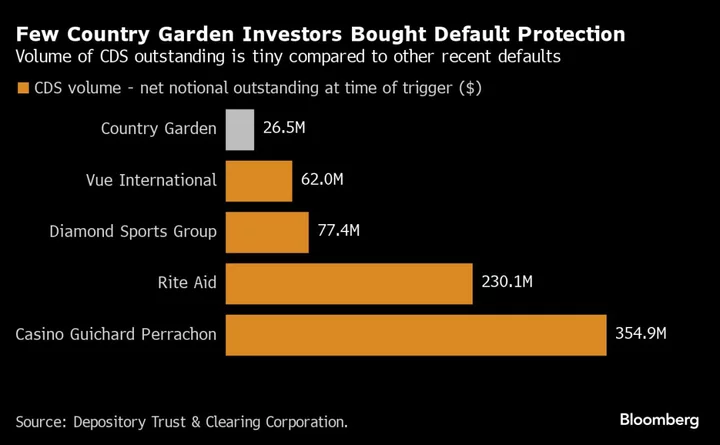

After a major default, investor attention usually turns to the potential payout from credit default swaps, a type of security that acts as insurance against bankruptcy. But when one of China’s biggest property developers missed a coupon on its bonds late last month, few bothered to check whether there would be any money up for grabs.

That’s because China’s CDS market is much less developed than in most major economies, meaning that many of the investors that bought Country Garden Holdings Ltd’s $10 billion of dollar bonds did so without hedging against default. The outstanding volume of swaps is so minuscule that the panel of dealers and investors which oversees the global CDS market ruled this week that it isn’t worth holding an auction to determine the size of a payout. Contracts will be settled bilaterally between buyers and sellers instead.

The lack of insurance is a further blow to investors who have faced a string of defaults in recent months as Chinese property firms struggle to pay back money borrowed when interest rates were much lower. The nation’s real estate developers still have around $160 billion in outstanding dollar bonds and not a single firm is included on a global list of 806 liquid CDS securities compiled by the Depository Trust & Clearing Corporation.

Resolving the collapse of China’s property market behemoths could take years, according to Carlos Casanova, a senior economist at Union Bancaire Privee in Hong Kong, and it’s likely to prove painful. “The restructuring of real estate sector debt will inevitably entail on-going defaults,” he said.

Credit default swaps never took off in Asia like they did in the US and Europe. In the early 2000s, China tried to build its own risk mitigation market, with securities that underpinned onshore bonds, but the market was fragmented and demand was weak for the instruments that function best in transparent, liquid markets.

Later, as China attempted to comply more with international standards, it tried to establish a CDS market for foreign-currency bonds but there wasn’t much interest since the volume of outstanding dollar debt was still quite small. When that debt load suddenly ballooned in the past decade, China’s low default rate meant that it didn’t matter much to investors that there was no safety net.

Read More: How China Is Reviving Tools for Hedging Credit Risk: QuickTake

As defaults pick up around the world due to rising interest rates, hedging is providing a lifeline for many investors. When French grocer Casino Guichard Perrachon SA defaulted on some coupon payments earlier this year, creditors who had bought CDS linked to the debt managed to recover 99% of the face value of their investment.

Investors in defaulted Chinese real estate issuers such as Sino-Ocean Group Holding Ltd, Powerlong Real Estate Holdings Ltd and Shimao Group Holdings Ltd weren’t so fortunate. In all three cases, the outstanding CDS volumes were so low that, as with Country Garden, no auction was held to determine a payout.

Holders of higher-quality Asian corporate debt can hedge using the Markit iTraxx Asia ex-Japan index which tracks CDS of 40 large investment-grade corporate and sovereign issuers in the region, but that doesn’t work as protection against high-yield bonds.

Some funds resort to using equity options as an alternative source of protection, according to investors interviewed by Bloomberg News. But that strategy also has its limits since shares of Chinese developers are often more volatile than their bond counterparts and not all companies with publicly listed bonds have listed equity. Another option is to buy bonds of one company and short stock of a peer.

Read more: How Country Garden Plays Into China’s Property Mess: QuickTake

--With assistance from Alice Huang.

(Updates with details of other Chinese real estate defaults in eighth graph.)